The past decade has been one of ‘exceptionalism’ for US equities as technological innovation has created a league of American superstar companies driving extraordinary equity gains. By comparison, the same decade has been described as ‘lost’ in emerging markets, which have been driven downward by uncompetitive currencies, failure to perform, property crashes and geopolitical conflicts.

Now, though, are we seeing strong signals the narrative is set to change? This article will outline why the time is right to invest in emerging markets as a results of green shoots in all regions – and, perhaps more importantly, why it is important to invest actively and with a different approach, tailored to the volatility of these markets, for greater success.

The decade-long relative underperformance of emerging markets is set to reverse. Following a traditional development trajectory, emerging markets should grow faster than developed one – but what is driving the current wide growth premium is the strength of the two largest markets, China and India.

China has consistently outgrown – even in the depths of the Covid-19 crisis, China delivered 2.2% growth. In the current environment of trade uncertainty, the US risks falling into recession, whereas China could maintain economic growth at 3% to 4% by raising its fiscal deficit and focusing on new infrastructure, domestic consumption and the recovery of the property market.

With 40% of China’s gross domestic product coming from consumption in 2024, further recovery in consumer confidence combined with government stimulus should keep a recovery on track. Future growth will be fuelled by the development of advanced technologies such as industrial automation, autonomous driving and artificial intelligence.

India, which now makes up almost 20% of the emerging markets index, is likely to deliver even higher growth of 5% to 6% due to rising consumption from an upwardly mobile population, capital expenditure driven by tax cuts, an improvement in rural demand and the proactive easing of rates. All of these conditions are supported by a skilled labour force, the strengthening of energy infrastructure and a shift of private savings into real estate and local equity investments.

Another leading economy poised for growth – albeit one that does not attract as much attention as the two giants – is Indonesia, where GDP could reach 4% to 5% over 2024 to 2026. With major companies in global agricultural commodities, mining and manufacturing and tourism, this country of 285 million people – with an average age of 30 – has domestic consumption and export potential.

Faced with external uncertainty, many emerging markets countries can shift their focus to domestic markets and the sector’s robust growth premium can be sustained by a large and growing middle class of consumers, governments with the leeway to provide fiscal stimulus and central banks that can cut interest rates.

“Investors are likely to benefit from diversification into emerging markets, which have lower valuations than the US and are experiencing unique domestic growth catalysts and structural changes.

Signs of global reallocation

The policy moves by President Trump’s administration on tariffs, immigration and the Department of Government Efficiency arguably pose a greater risk to the US than to emerging-market countries, due to the inflationary pressures and negative economic growth shock they are likely to bring.

The US ‘exceptionalism’ narrative is fading and, with the weakening of the dollar, emerging markets should outperform the US – yet, at the same time, emerging-market countries are currently significantly under-owned by global investors.

As the US market sells off, then, investors are likely to benefit from diversification into emerging markets, which have lower valuations than the US and are experiencing unique domestic growth catalysts and structural changes such as urbanisation, youthful populations and an expanding middle class – all relatively unaffected by global factors.

There are signs of a global reallocation in a new world order. On the matter of valuations, even following the pullback earlier this year, US equity markets have been trading at high valuations of around 20x earnings. Conversely, since the US presidential election, emerging markets equities have dropped to below 12x earnings. Relative valuations versus the US have been at historical lows – and at discounts greater than 40%.

Rapid levelling-up

Technological innovation, infrastructure development and industrial upgrades all lie at the heart of emerging-market economies – and investing in these themes could bring multi-year gains. These are vibrant, rapidly growing economies with strong intellectual capital and which do not need the US or other developed markets to create their own new products or technology – as demonstrated by the unveiling of China’s DeepSeek AI technology earlier this year.

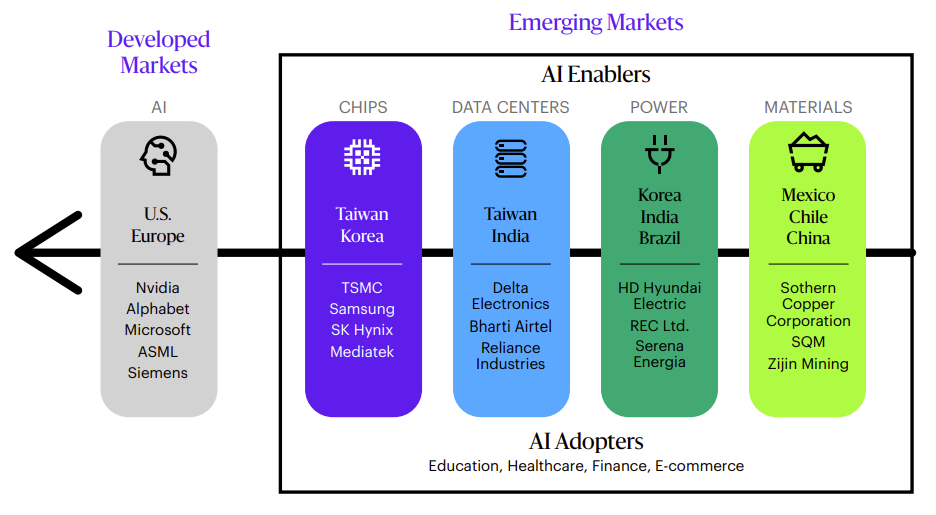

As the diagram below illustrates, emerging markets countries are arguably well-prepared for the AI revolution: Taiwan and Korea are the world’s leading chip manufacturers and Taiwan and India are home to major data centres, while the power and raw materials to fuel the AI revolution will come from countries such as Korea, India, Mexico and China.

Fintech, healthcare, telecommunications and medical equipment – these are all areas where rapid innovation and development are obvious within the emerging markets and all sectors where AI is likely to be rapidly integrated and boost growth opportunities. Consumer staples are also an important emerging-market investment theme, as are commodities and materials, such as gold, silver, copper and oil.

Source: Allspring - for illustrative purposes only

Coping with EM volatility

There can be no doubt that investing in emerging markets comes with heightened risks for investors, including greater volatility and reaction to news and current events. Emerging-market currencies can also depreciate more suddenly and more rapidly while countries can be more susceptible to political instability. There can also be risks around regulatory uncertainty and the difficulties in enforcing contracts and reporting on environmental, social and governance concerns.

The key to mitigating these risks is active and highly selective investment. Research by MSCI backs up our own experience that active investment with a risk-adjusted, total-return approach is the most effective way to invest in emerging markets over the long term. This approach considers top-down risks and the bottom-up fundamentals with the aim of creating a resilient portfolio able to generate alpha and outperform over the cycle.

For our part, we focus on assessing the macroeconomic and political risks in each country and evaluate each sector and industry. Then, for security selection, we look at shareholder yield – including cash dividends, stock buybacks and spin-offs – as well as capital appreciation to identify quality companies, generate returns and protect against downside risk.

Additionally, deep fundamental and ESG analysis is crucial, and we invest in companies we believe offer the best risk-adjusted upside. In our experience, if companies are quality and liquid, they are more likely to ride through any short-term turbulence, which is why proper and active stock selection is so important. It influences the countries, sectors and companies we choose to invest in.

And, according to the MSCI paper Long-Term Investing in the Emerging Markets, a company’s profitability; investment quality; and, above all, dividend yield are all more important to long-term compounding stocks than the company’s growth trajectory.

Emerging markets can provide growth and income. The low coverage of regions by analysts means there are opportunities for managers who focus on key fundamentals and capital return policies and who take a systematic approach across companies of quality. Historically, these have all been investment approaches that have contributed to outpacing broader emerging markets benchmarks.

There is currently an opportunity for investors to diversify into emerging markets when the first signs of an exceptional decade are beginning to appear. We expect to see money moving in a significant way from developed to emerging investments in the period ahead – indeed, we might even go so far as to say this is the decade in which many of the so-called emerging markets countries will fully emerge.

Alison Shimada is a senior portfolio manager and head of total emerging markets equity at Allspring