The concept of ‘service’ is rather a nebulous one. In my experience, a client’s sensitivity to service issues is inextricably linked to the investment outcomes they are experiencing. If investments are doing well, a few service issues can be forgiven; on the other hand, if investments are not delivering or are going through a rather extended downturn, then the importance of these service issues is magnified.

This market-movement bias does not apply so much to financial advisers, who rely on efficiency and support from their selected providers, regardless of outcomes. Any drop in service standards affects their ability to do business.

This is quite an important distinction as at Defaqto, focusing on the advised market, we look at discretionary investment primarily as an advised solution. When we look at DFM service, we therefore assess it as a service to the adviser, acting on behalf of the client.

Defaqto started analysing the discretionary market in 2010, as it seemed clear that discretionary management was an obvious alternative to multi-manager fund investing for those advisers who were going to be ‘guided’ by the regulators into outsourcing their clients’ investments to specialist asset managers.

We have come a long way in service assessment since those early days, when many discretionary managers genuinely did not understand why advisers would want to know ‘minor’ details such as charges, what the portfolios were investing in, what risk measures were in place – or, for that matter, performance.

Increasing burden

Many DFMs were still focusing primarily on giving the client a good experience, with perhaps an annual lunch in the fabled oak-panelled boardroom having served them well in the past – in some cases for centuries. The burden on advisers to justify recommendations was increasing, however, and this kind of approach would no longer be acceptable.

If the DFMs had any hope of taking a slice of the outsourcing market, advisers needed information, support and a good service from discretionary managers. Defaqto cultivated good relationships over the years following RDR and we have been able to supply advisers with the information they needed.

As part of this provision to advisers, since 2015 we have been running an annual satisfaction study with advisers to ascertain what is important to them, and how their preferred DFM providers stack up. We are thus able to produce an annual set of service ratings based on the overall service provided by qualifying discretionary managers – that is to say, at least 10 adviser responses and excluding those tied to a discretionary manager.

It is important to note the rating is based on the service provided by the discretionary firm overall and not specifically on any one proposition, whether bespoke, MPS direct or MPS on a platform.

Incidentally, including MPS on a platform is quite an about-turn in the study in that, immediately post-RDR, there was some concern about DFMs poaching advisers’ clients. Of course, the contractual arrangements for MPS portfolios on a platform meant the discretionary manager was at least one stage removed from the client and did not necessarily know any client details.

As the market grew and advisers and discretionary managers became familiar with each other, however, this worry disappeared. Perhaps over the last 10 years or so, advisers realised they required just as much support for themselves and their clients as they do for other products and services. Advisers now value the service offered to them regardless of the discretionary proposition type.

“We have come a long way since the days when many discretionary managers genuinely did not understand why advisers would want to know ‘minor’ details such as charges – or even performance.

Service disciplines

Every year Defaqto undertakes a satisfaction study among advisers, firstly asking them to tell us how importantly, on a scale of 1 to 5, they rate the following service disciplines:

New business servicing: Ease and efficiency in processing new applications. Applications are processed accurately within agreed timescales and systems; and processes to move existing clients’ investment portfolios are efficient.

Existing business administration: Efficiency of processing product changes after inception. Provider responds quickly and accurately to enquiries and within agreed timescales for reports, switching, statements and valuations. Cash management, flexibility of income payments, capital gains tax management.

Reporting: Online portfolio reporting, trading activity and investment reports are clearly laid out and accurate; plus business reporting on client activity, transaction progress and remuneration is clear, concise and comprehensive.

Online facilities: Up-to-date portfolio information and management, valuations, transactions and transaction histories are available to the adviser. Capability to complete online transactions for new business as well as increments is available and easy to use. IT technical support, system reliability and access as well as general website functionality.

Accessibility: Availability of the DFM service through third-party platforms and other tax wrappers – for example, ISA, offshore bond or SIPP – is compatible with the current ‘buy list’.

Quality of staff – administration: DFM staff are available and able to deal with a range of enquiries, bringing them to a satisfactory conclusion and in a timely manner.

Quality of staff – investment: Investment managers or account managers are able to respond to any investment queries with knowledge and conviction, accurately reflecting any current portfolio positions or market views. Ability to support the adviser firm in promoting the service.

Quality of literature: Clear, easy-to-understand literature and terms that give advisers and clients a fair representation of the service they should expect.

From all of that, we calculate a mean score out of five to determine the importance of each individual aspect of service. We then measure the adviser’s satisfaction levels with their preferred DFM providers.

Next, these results are weighted by the importance of each category and aggregated to determine one overall satisfaction rating for each preferred provider. The highest award is ‘Gold’ and, as well as an overall rating, the score for each individual category is available through Defaqto Engage software.

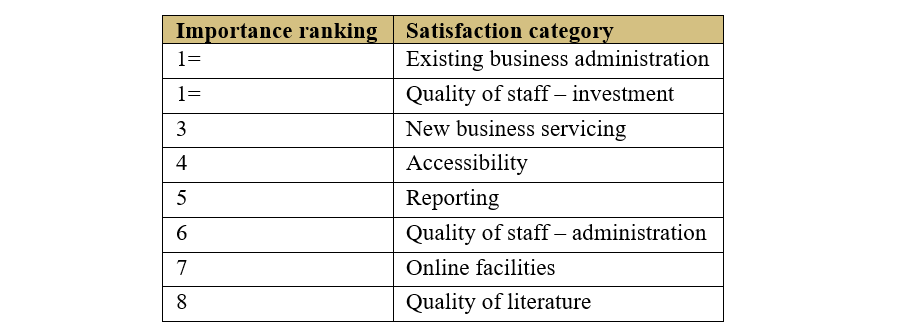

For the latest study, published earlier this year, the order of importance to advisers was as follows:

Source: Defaqto

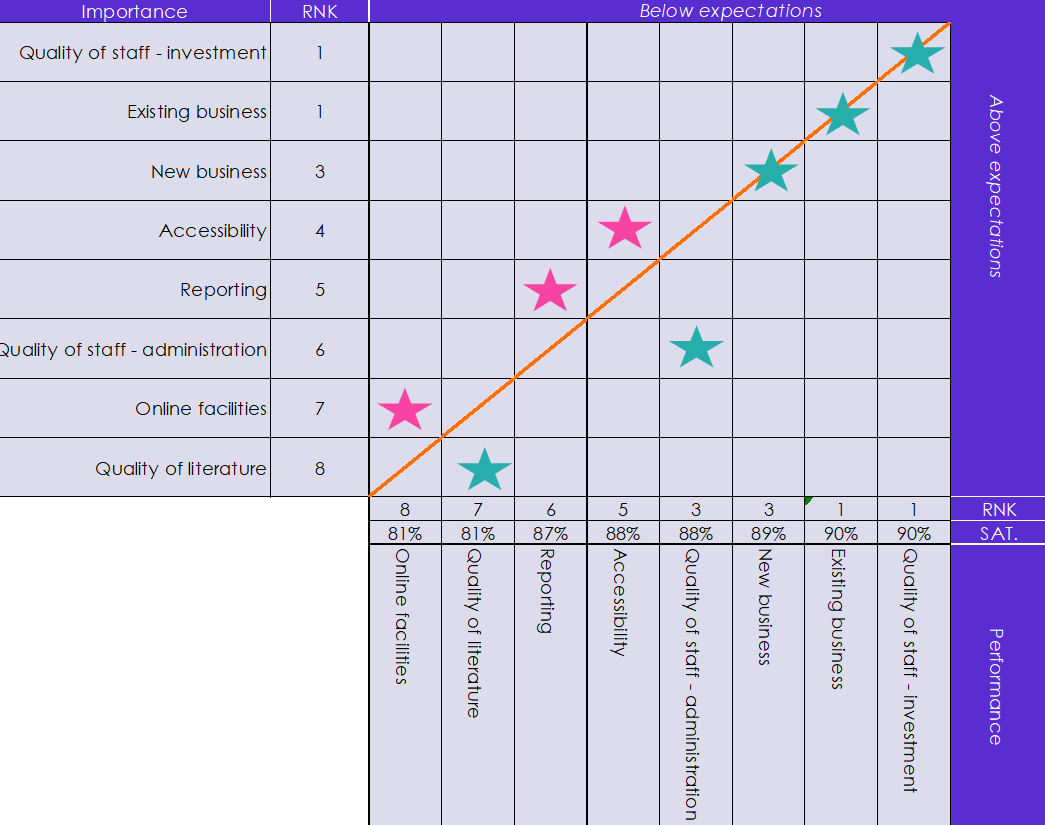

Regardless of position, the importance of each category to advisers is high – all score well over 4 out of 5. Nonetheless if we look at the chart below, it is noticeable that despite the high level of importance placed on each category, the industry as a whole is meeting adviser expectations in all but three of the categories. Importantly, all of the top three most important categories are meeting expectations:

Source: Defaqto

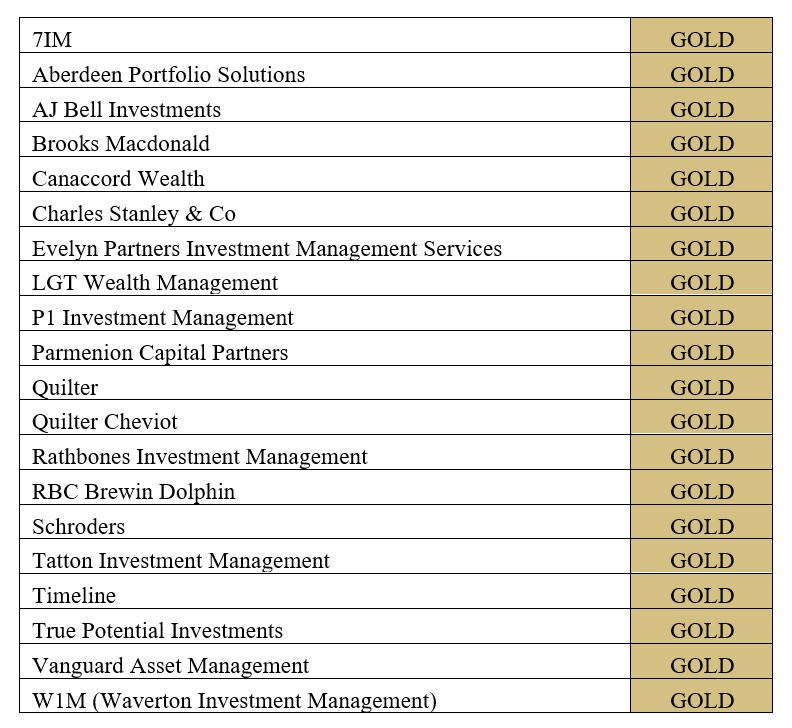

The DFMs from the current vintage that achieved a Gold Service Rating are as follows:

Source: Defaqto

Each year, the study is carried out across between 300 and 500 advisers and, with individual category scores also accessible through Defaqto Engage, advisers can check to see where their peers rate DFM businesses more highly.

It is also worth noting there will be a number of providers not listed above that will have achieved ‘Gold’ standard service but may have been excluded as we received an insufficient number of responses for the provider. We would certainly expect the above list to expand as more DFMs become established and gain traction in the adviser market.

Overall though, and ratings aside, at Defaqto we feel this study is incredibly important to the industry. Competition in the DFM space continues to increase and business retention is crucial. DFMs should be paying attention to what is important to advisers – and hence where they may feel some improvement can be implemented. In the chart above, we can see accessibility, reporting and online facilities are currently falling a little short of expectations.

Andy Parsons is head of investments at Defaqto