Tail risk is one of the most important yet persistently underestimated concepts in investing. Markets spend most of their time rewarding consistency, optimism and participation. As such, long periods of relatively stable returns encourage investors to believe diversification, historical averages and broad market exposure are sufficient to navigate uncertainty.

And yet the greatest damage to portfolios rarely comes from ordinary market volatility. Instead, it comes from extreme events – sudden dislocations that sit outside normal expectations and fundamentally alter both investor behaviour and market structure.

These are known as ‘tail events’ and, while they occur infrequently, when they arrive they reshape investment outcomes far more than day-to-day fluctuations ever could. The global financial crisis, the pandemic-driven market collapse, inflation shocks, sovereign debt crises and sudden geopolitical escalations all serve as reminders that markets are far more fragile than they often appear during periods of calm.

What makes tail risk damaging is not simply the magnitude of losses it can create, it is also the way it exposes the weaknesses embedded in conventional portfolio construction.

Today, this issue feels increasingly relevant. Equity markets continue to climb, supported by enthusiasm around artificial intelligence, resilient corporate earnings and the assumption that innovation and liquidity will continue to underpin growth.

“Resilience has become a central objective in portfolio construction. The aim is not to eliminate risk, but to build portfolios capable of withstanding a wider range of scenarios.

Investors who believe they can tolerate volatility in theory frequently discover their actual tolerance for loss is far lower in practice.”

Beneath this optimism, however, sits a much more uncertain reality. Geopolitical tensions are intensifying, global alliances are shifting, economic fragmentation is accelerating and financial markets themselves are becoming more interconnected and reactive. In many ways, markets are simultaneously exhibiting confidence on the surface while carrying deeper structural vulnerabilities underneath.

There is thus greater demand among investors to protect portfolios from tail risk – particularly because extreme market events tend to occur when we are least prepared. Periods of low volatility often encourage leverage, concentration, and complacency, creating a false sense of stability. Yet financial history shows that prolonged stability can itself create fragility, leaving portfolios increasingly vulnerable to sudden reversals.

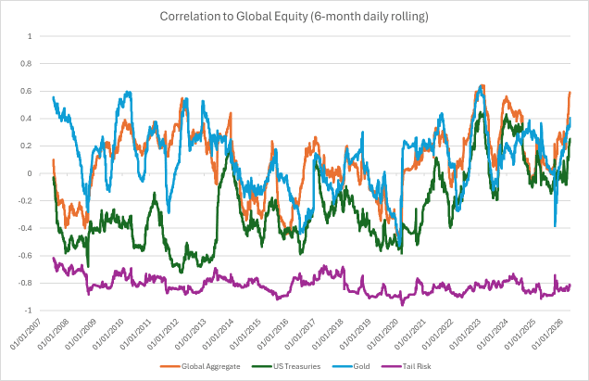

Traditional diversification may also no longer offer the same protection investors once relied upon. For decades, balanced portfolios benefitted from the negative correlation between equities and government bonds. When equities sold off, bonds typically rallied, helping cushion portfolio losses – and yet recent market environments have challenged that assumption.

Inflationary pressures and rising interest rates have shown bonds can decline alongside equities, undermining one of the foundational principles of traditional portfolio construction. Other traditional defensive assets, including gold, have at times delivered inconsistent protection during periods of stress. This has created an uncomfortable reality for investors: many portfolios may be less resilient than they appear.

Correlations of selected assets to global equity

Source: Bloomberg, 01/01/07 to 06/02/26

Tail risk is not simply about market losses in isolation – its real impact often emerges through investor behaviour. Large drawdowns change decision-making. They create fear, uncertainty and the temptation to abandon long-term strategies at precisely the wrong moment.

Investors who believe they can tolerate volatility in theory frequently discover that their actual tolerance for loss is far lower in practice. Selling near market bottoms, reducing exposure after sharp declines or abandoning investment plans entirely can permanently impair long-term returns. In many cases, the behavioural consequences of tail events become more damaging than the events themselves.

Resilience has become a central objective in portfolio construction. The aim is not to eliminate risk, but to build portfolios capable of withstanding a wider range of scenarios. Investors increasingly recognise that maximising returns is insufficient if the risks involved can permanently impair capital or discipline.

Extreme events are not anomalies – they are an unavoidable feature of markets.”

Tail risk strategies are evolving beyond standalone hedges. They are now being integrated into broader portfolios as diversifiers, stabilisers and potential sources of return. This reflects a broader shift in thinking: volatility is no longer viewed as a temporary disruption but as a structural feature of modern markets.

The geopolitical backdrop reinforces this reality. Rising competition over technology, energy, semiconductors and artificial intelligence is embedding uncertainty more deeply into financial systems. Extreme events are therefore not anomalies – they are an unavoidable feature of markets.

The challenge is not predicting the next dislocation but building portfolios resilient enough to endure it. The most successful investors over the coming decade are likely to be those who prioritise resilience, manage fragility and prepare for extreme outcomes alongside growth.

Tom May is global CIO, outcome and derivative strategies at Atlantic House. An asset manager specialising in risk-managed derivative solutions, it is now part of WisdomTree