Investment banker and former Goldman Sachs CEO Lloyd Blankfein recently observed that the US economy feels “late cycle” – an assessment that resonates and one that should be noted by investors everywhere.

Historically, late-cycle regimes are notoriously less forgiving. Financial conditions tighten, refinancing risks rise and the earnings leadership that sustained the previous bull run begins to rotate. At this stage of the cycle, complacency is rarely rewarded.

For much of the past decade, investing felt deceptively straightforward (not to mention, for believers in active management, somewhat frustrating). Passive exposure delivered strong returns, US equities dominated global indices, and a narrow group of mega-cap technology stocks drove both the performance and the narrative.

Market weakness was brief, liquidity was abundant and central banks were predictable. In that environment, the ‘buy the dip’ mentality became cultish in its intensity – a collective suspension of disbelief that rewarded blind momentum and punished anyone still concerned with valuations.

Easy come, not so easy go?

It has, in many respects, been too easy – but late cycles change the rules. Growth is moderating, inflation remains uneven and fiscal deficits are elevated. We are witnessing monetary policy move in divergence rather than lockstep, as the Fed, the ECB and the Bank of England navigate differing domestic pressures. What we are experiencing is not simply a bout of volatility – it is a meaningful, structural shift in regime.

While this shift should not be feared, though, it must be respected and embraced. Periods of greater differentiation and more normalised volatility maybe uncomfortable for those used to the sedative of the post-GFC era yet they are also constructive.

Opportunity is no longer concentrated in a single theme, relative value is returning and company-specific fundamentals matter again. This is the environment in which alpha can be found in plentiful supply – and therefore the perfect environment for absolute return strategies to thrive.

Faced with uncertainty, the instinct is often to revert to familiar tools: reduce equity exposure and extend duration as a ‘flight to safety.’ That approach worked when falling inflation and aggressive rate cuts made duration a powerful hedge – however, the current backdrop is fundamentally messier.

Duration is no longer a guaranteed one-way hedge and carries significant risk if the ‘higher for longer’ structural pressures persist. Similarly, corporate credit can feel defensive yet tight spreads offer a limited margin for error. When growth slows and refinancing pressures rise, the income yield can quickly be offset by widening spreads. The tools remain familiar but the environment has changed – investors are effectively using a map of the 2010s to navigate the terrain of the 2020s.

Illiquidity is not ‘safety’

Investors have recently sought diversification through increased allocations to private credit, infrastructure and private equity. Many, however, have been seduced by the smoothing effect of private markets – and here lies the potential for some disappointment.

While the surface remains calm enough, the first undercurrents are appearing in private markets via suspended redemptions and rising default warnings. This is potentially a problem for tomorrow, not today, but investors should be very wary of illiquidity right now.

Illiquidity does not remove risk, it merely delays its recognition. This ‘mark-to-model’ mirage (and sometimes, let’s be honest, it is even ‘marked-to-myth’) suggests that if we do not observe a price movement, the value of an asset has not changed.

We saw this before the 2008 crisis, when many structured instruments were considered stable – until funding conditions tightened. In a late-cycle environment that tests balance sheets and exposes leverage, flexibility – the ability to rebalance, hedge and adjust in real time – is an undervalued asset. Illiquidity removes that option exactly when it is needed most.

Finally … the good news

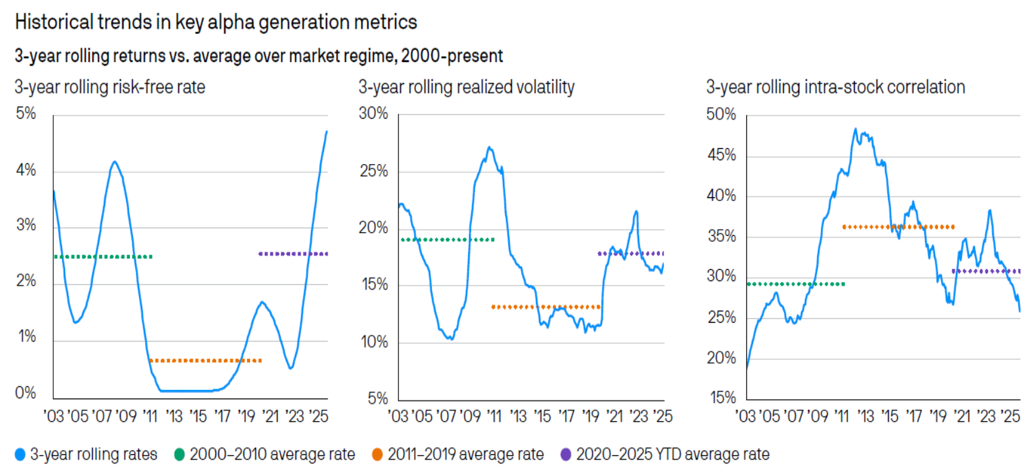

To understand why alpha managers are witnessing their most compelling opportunity set in over a decade, we must look at the structural decay of the post-GFC ‘goldilocks’ environment. Research from J.P. Morgan Asset Management highlights three distinct structural pillars that have moved in favour of alpha generation, which underpins absolute return strategies:

* Return of the hurdle rate: As the first of the three graphs below illustrates, between 2011 and 2019, the three-year rolling risk-free rate averaged roughly 0.6%. Today, that rate has surged toward 5%, with the 2020/25 average resetting to 2.5%. The impact? Cash finally offers a decent hurdle rate which, when combined with alpha generation, creates a compounding effect that allows investors finally to capture a meaningful absolute return.

* Normalisation of realised volatility: Post-GFC, volatility was artificially dampened, averaging just 13.2%. As the middle graph below shows, we have since seen a breakout, with the 2020/25 average rising to 17.8%. The impact? A higher level of realised volatility is not a ‘crisis’ – it is a market functioning without the stabilisers of a toddler’s bike. It creates the price movement necessary for active managers to enter and exit positions at attractive valuations.

* Breakdown of correlation: As the third graph below illustrates, the three-year rolling intra-stock correlation has dropped from a previous decade peak of 36.3% to a current average of 30.8%. The impact? In the passive boom, a rising tide lifted all boats. Today, stocks are behaving more independently. This widening dispersion allows managers to harvest idiosyncratic risk by going long on quality and short on laggards.

Historical trends in key alpha-generation metrics

“The tools remain familiar but the environment has changed – investors are effectively using a map of the 2010s to navigate the terrain of the 2020s.

Source: Bloomberg, J.P. Morgan Alternative Solutions, J.P. Morgan Asset Management; as of June 2025. Volatility: realised 30-day SPX volatility; intra-stock correlation; one-month intra-stock SPY correlation; and risk-free rate: three-month T-bills

The era of the narrow market, where a handful of giant stocks effectively were the world’s stockmarket, has reached its logical conclusion. In its place, we are witnessing a regime break: the birth of a more typical, dispersed and uncorrelated financial landscape.

While traditional portfolios suffer from systematic beta that drags all boats down, absolute return strategies thrive on idiosyncratic risk – the risk specific to an individual asset, uncoupled from macro noise. By going both long and short, managers put themselves in a position to harvest these specific opportunities, regardless of the direction of the S&P 500 or the FTSE 100.

As correlations break down, diversification returns. We are seeing policy divergence between nations and performance divergence between companies. In this environment, the ability to bet on a winner while simultaneously hedging against a loser is the only way to generate true, uncorrelated returns. Uncertainty does not eliminate opportunity – in the absolute return asset class, it enhances the toolkit.

Making uncertainty work for clients

Liquid alternatives struggled during the liquidity-suppressed decade where scale mattered more than selectivity. As macro conditions become less predictable, however, simply owning the index is no longer enough. Policy divergence and refinancing pressures introduce a level of complexity to which passive vehicles cannot adapt.

Active managers are starting to see outperformance and, within that cohort, absolute return managers are thriving. These strategies are designed for markets where differentiation and dynamic risk management are the primary drivers of return. They do not rely on falling rates or expanding multiples – they are built to operate within volatility, not wait for it to subside.

The dominance of the passive era may end not so much end with a bang as a whimper as the conditions that sustained it evaporate. Zero rates, suppressed volatility and elevated correlation formed a powerful tailwind that has now turned into a headwind. Incorporating liquid alternatives is not a rejection of passive investing – it is a recognition that, as regimes evolve, diversification must evolve with them.

Macro complexity reinforces this shift. Monetary policy is no longer synchronised – fiscal dynamics differ materially between economies. These forces introduce dispersion not just within equities, but across currencies, yield curves and credit markets. Strategies capable of navigating across asset classes and exploiting relative moves are inherently better suited to this environment than static allocations designed for uniform policy.

For asset allocators willing to look beyond what has worked for the last 15 years, this is a meaningful moment. We are moving into a more disciplined, more differentiated environment where volatility creates entry points and mispricing becomes more visible. This is precisely the backdrop in which alpha and the targeting of idiosyncratic risk can flourish.

The real question is no longer whether uncertainty exists – it is whether your portfolios are built to make use of it.

Ian Willings is a portfolio manager and partner at Apollo Multi Asset Management, experts in researching and investing in absolute return and liquid alternative strategies. CIO, Steve Brann, is the author of Absolute Vision, a book that sets out the thinking behind the firm’s strategy and looks to demystify the asset class for a wider audience.