Two decades ago, sectors such as data centres, industrial, senior housing and self-storage, as well as newer categories such as single-family rentals and towers, were small pieces of the real estate investment universe.

These sectors, collectively referred to as ‘next gen real estate’, have expanded to more than half the market today – from 17% of a total $172bn (£128bn) of assets in 2003 to 58% of $1.4tn in 2025 – and it is not just the growth in size of this grouping that is remarkable either.

What is also worth noting is the growth in the importance of these sectors. Today, these businesses sit at the centre of the modern economy while benefitting from notable secular changes – from the rise of AI, cloud computing and e-commerce to large-scale demographic shifts.

The reason 2026 set up to be a strong year for REITs is down to two things happening at the same time. First, next gen real estate has powerful, long-run tailwinds, such as AI infrastructure, data proliferation and e-commerce supply chains, as well as population shifts from both aging demographics and the demand drivers from the large Gen Z population. Those dynamics are not cyclical but structural.

Second, coming into 2026, the broader real estate environment has been turning increasingly supportive. As a firm, we are above consensus expectations for economic growth and inflation and expect stable interest rates. Combined with a more accommodative monetary policy, such conditions have historically favoured real estate. Valuations have reset and liquidity needs are driving greater listed allocations.

“Today, these businesses sit at the centre of the modern economy while benefitting from notable secular changes – from the rise of AI, cloud computing and e-commerce to large-scale demographic shifts.

Data centres underperformed in 2025 despite massive AI-driven capital expenditure by large tech companies. Nevertheless, the underlying trend has not changed.”

We also expect economic activity and market returns to broaden after several years of highly concentrated gains, moving away from the so-called ‘K-shaped’ recovery that favoured only certain stocks to a broader recovery that, among other allocations, will favour real estate.

Overall, as investors, we favour assets that have strong secular growth profiles and good pricing power. It is these same attributes that have driven the rapid growth of next-gen real estate for a couple of decades now.

This year, next gen sectors should continue to be positioned for leadership. Supply remains constrained for many of these property types, while demand is accelerating, with key trends driving that demand.

Two sectors in particular stand out – data centres and senior housing. Data centres underperformed in 2025 despite massive AI-driven capital expenditure by large tech companies. Investors preferred direct tech stocks over data centre REITs as they looked to invest in the AI trend.

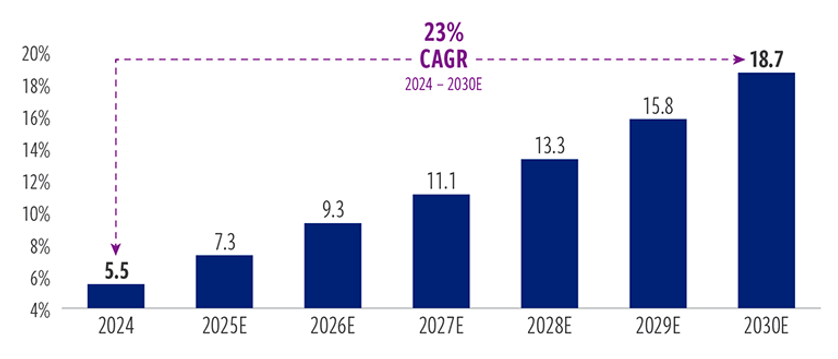

DeepSeek concerns hit the market first, then a key tech firm paused new leasing … and then several operators ran out of available power capacity, creating short term questions about the sector. Nevertheless, the underlying trend has not changed. If anything, it has strengthened amid the underperformance last year – and, as the following chart illustrates, AI related data demand is projected to grow more than 20% annually through to 2030. Global AI data centre demand (Gw)

Source: Cohen & Steers; 2024-2030E

At the same time, rents continue to rise, development margins remain healthy and REITs have been deploying capital into power constrained, high value markets where pricing power is strongest. Yes – month to month headlines may fluctuate, but the fundamentals remain one of the most attractive secular growth stories in global real estate.

As for senior housing, an imbalance of surging demand and limited supply is driving higher occupancy and improved rental growth. Senior housing operators are consolidating, cost pressures are easing and the sector is experiencing its most sustained recovery in years. Put simply, both the demographic math and the competitive dynamics are improving.

The main risk here is future supply growth if construction costs fall or new entrants emerge. That said, new supply will take time to have an impact and, in the meantime, we will have several more years of baby-boomers turning 80.

Combine the favourable 2026 environment for real estate overall with the powerful secular growth behind next generation sectors and a 2025 reset that has created clear valuation and performance dispersion, and you end up with one of the most supportive backdrops for real estate investing we have seen in years.

Seth Laughlin is head of real estate strategy & research at Cohen & Steers