The US is still home to the world’s largest economy and its reserve currency, as well as the globe’s largest equity and bond markets, but investors continue to reassess their exposure one year on from Liberation Day.

Tariffs and strong-arm trade tactics, challenges to the independence of the Federal Reserve and now military incursions in Latin America and the Middle East, as well as sabre-rattling over Greenland, are combining with lofty American stockmarket valuations and a soaring Federal deficit and prompting investors to reassess the narrative of ‘American exceptionalism’.

Donald Trump’s first term in the White House made it clear he was a firm believer in tariffs. In early 2018, America’s 45th president imposed levies on a range of goods – from solar panels to steel and washing machines to aluminium –not just on China, but on purported trade partners and allies such as Canada, Mexico and the EU.

Retaliatory tariffs and negotiations prompted the withdrawal of some of these tariffs, but the Biden administration added to the range of levies on Chinese goods and the second Trump presidency took the trade policy to a whole new level on 2 April 2025 with his so-called 10% baseline and additional reciprocal tariffs on pretty much all goods imported by America.

Neither stock nor bond markets welcomed the policy, despite – or perhaps because of – Trump’s claim that the result would be good for American jobs as it would encourage manufacturers to build new factories in the US, good for US consumers and good for the Federal deficit, thanks to the taxation income generated.

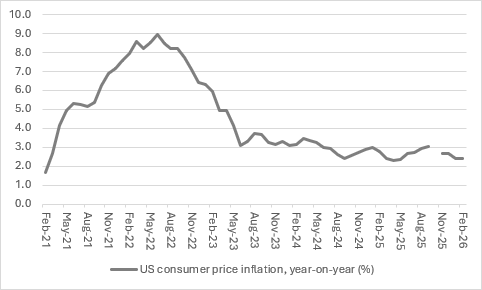

Some of these goals seemed incompatible – if not downright contradictory – but US growth did not take a hit and nor did inflation career higher. The April round of tariffs would have taken the overall level of US tariffs on imported goods to the highest in a century at almost 30%, but individually-brokered trade deals, including with the EU and UK, a pause on tariffs on Chinese goods and then the nullification of some of the levies by the US Supreme Court means the prevailing rate is around 10%, according to the Yale Budget Lab. That compares with 2.4% before Liberation Day.

Tax income from tariffs rocketed but the debate over who ultimately pays was not settled. Trump insists the foreigner pays. American companies are yet to show margin pressure but many believe the US consumer ultimately takes the hit through higher prices.

US importers had a chance to prepare and build stock last year, but those inventories may now be depleted and perhaps 2026 will be the year when any effect upon prices or corporate profit margins starts to become apparent.

“Investors do seem to have thought carefully about where to allocate capital in a post-Liberation Day world – and one where presidential social media posts carry heft politically, economically and militarily.

Source: FRED – St. Louis Federal Reserve database

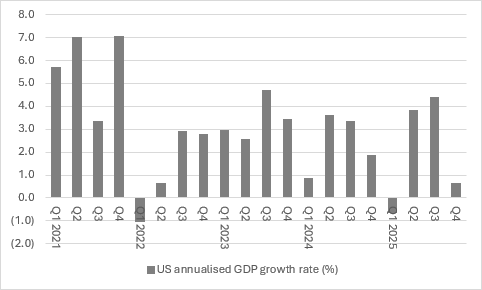

The war in the Middle East could mean that tracking the effects of tariffs is harder than ever, while the dip in GDP growth in the final three months of 2025 may owe as much to the US government shutdown and budget stand-off on Capitol Hill as anything else.

But any sign of higher prices and slower growth could yet be a lingering effect of the tariffs – at least those imposed under section 301 of the 1974 Trade Act that remains in force. It does at least seem likely that preparations for, and responses to, tariffs had something to do with the volatile trends in US GDP growth in 2025.

Source: FRED - St. Louis Federal Reserve database

Asset classes

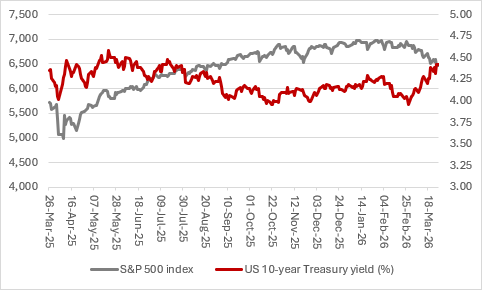

US and global stock and bond markets rebounded quickly as Trump backed off from the maximum level of reciprocal tariffs imposed and investors decided the worst-case scenario of a global trade war was priced in, but unlikely to materialise. Share prices rose and benchmark bond yields retreated.

Source: LSEG Refinitiv data

Investors do seem, however, to have thought carefully about where to allocate capital in a post-Liberation Day world – and one where presidential social media posts carry heft politically, economically and militarily.

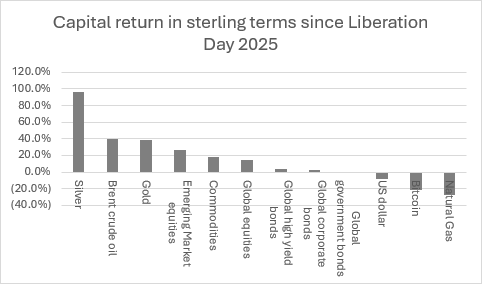

Bonds have done badly and, although equities have recovered, commodities have outpaced them. This perhaps reflects how Covid-19, tariffs and wars in the Middle East and Eastern Europe place fresh emphasis on supply chains and reliable sources of vital materials as a key part of national and economic security.

Gold and silver have led the charge, owing to fears of inflation, or stagflation – concerns that have also weighed heavily on bonds. Oil’s gains owe much to the war in the Middle East, but that is serving to cement the outperformance of raw materials relative to equities or bonds.

Dollar weakness has also fed into higher commodity prices, since most raw materials are priced in greenbacks and thus become cheaper in local currency terms for non-dollar uses. A lower US currency is also usually a boon for emerging markets, some of whom are also leading commodity producers.

Many developing nations borrow in dollars, so a weaker buck makes it easier for them to service the interest bill and repay principal – freeing up cash for investment elsewhere in their domestic economies.

Source: LSEG Refinitiv data. To 26/03/26

Equity markets

Equity and bond markets have lagged commodities as investors have considered the importance of supply chains. President Trump’s intervention in Venezuela, the tit-for-tat dispute with China over rare earth minerals and even whether the American military assault on Iran has a lasting impact on oil and Tehran’s role as a major supplier to Beijing are among the many strategic considerations.

In addition, the US stockmarket may have bounced back strongly from the Liberation Day low, but it has not been the first destination of choice, as had been the case for most of the time since the conclusion of the Great Financial Crisis in 2009. In other words, it is no longer a case of ‘America first and the rest nowhere’.

Source: LSEG Refinitiv data. To 26/03/26

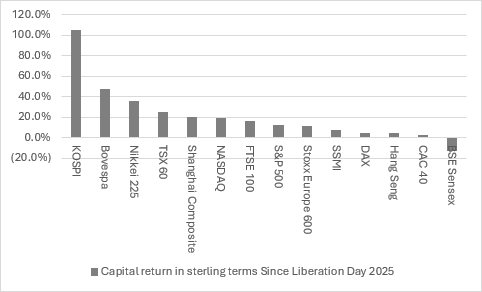

Emerging markets have led the charge in the shape of Korea, thanks to plenty of technology and artificial intelligence magic dust, and Brazil, which is rich in commodities – a facet which also explains the prominent showing of Canada’s TSX60 in the global rankings.

Impressive returns from Japan and China owe much to fiscal or monetary stimulus and attractive starting points from a valuation point of view – a feature America cannot offer after its stunning outperformance since 2009.

And the much-maligned FTSE 100 has edged ahead of the more lauded S&P 500. The UK index is benefiting from its relatively low exposure to richly valued technology stocks – where investors appear no longer sure whether AI is a threat or an opportunity – and heavier weightings toward commodities through its brigade of miners and oil and gas producers.

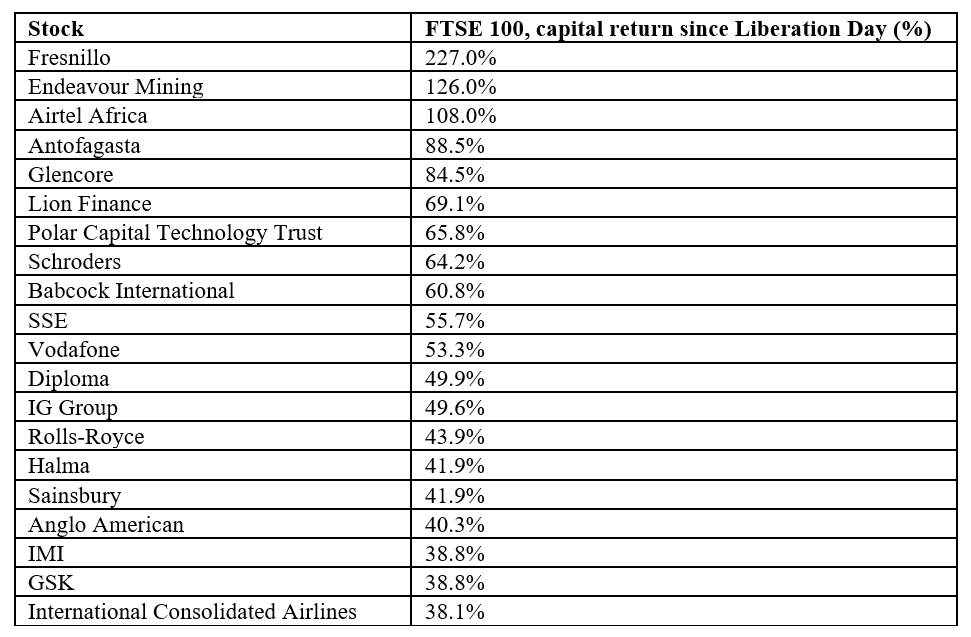

These trends can be seen at stock level, in the list below of the 20 best performers within the current FTSE 100 constituent list. Four of the top six performers are miners and the other two, in the form of Airtel Africa and Lion Finance, are emerging market plays.

Russ Mould is investment director at AJ Bell

Source: LSEG Refinitiv data. To 26/03/26