It has been an interesting few months in the world of discretionary management as the Financial Conduct Authority begins its analysis of the model portfolio service sector.

Through the publication of the MPS multi-firm review survey, the regulator is seeking to build a picture of the shape of the market, asking DFMs about their approach and practices to elements of running MPS ranges.

The review was signposted early last year and became one of the priorities mentioned in the FCA annual Regulatory Priorities report for consumer investments, confirming the regulator will progress its review of MPS firms during 2026.

The outcome of the review will likely be guidance on good and bad practices regarding Fair Value and the implementation and embedding of Consumer Duty in order that customers are treated fairly and have the best possible chance of good outcomes.

Since the Retail Distribution Review, we have seen a succession of regulation designed to put the client at the heart of decision-making and ensure they are being treated fairly – albeit this has predominantly been focused on more traditional formally-structured investment entities, such as Oeics and unit trusts.

2012 saw detailed guidance on assessing suitability, which certainly hit home and has been the standard since. Assessment of Value was introduced in 2018, encouraging asset managers to look at their investment offerings and assess whether they were good value. In the MPS market, take-up was slow and there was often little hard data to back up firm’s conclusions that their portfolio offerings were indeed fair value.

In essence, there was a general cynicism over the process – in that advisers felt that asset managers ‘marking their own homework’ had a kind of built-in conflict of interest – which was not helped by the general lack of information in the early assessments. It is fair to say that these assessments have improved considerably over the last few years.

Industry shortcomings

We next come to Consumer Duty, which was introduced in 2023. This was a new outcomes-based regulatory framework that focused on four areas: product and service, price and value, consumer understanding and consumer support.

Again, this framework is all about Treating Customers Fairly – and, while it would be fair to say that all these elements should already be in place, it is clear the FCA felt there were shortcomings in the industry and that it had to spell out its expectations with this new framework.

And now we are at the MPS review mentioned above. We have seen enormous growth in this sector – to the point that MPS portfolio investment is now almost on a par with multi-asset fund investing. It is clear the FCA still sees shortcomings in this sector and the current review will spell out its expectations along with good and poor practice examples.

Just to be absolutely clear, this is a review advisers need to pay close attention to so they can ensure their preferred DFMs have been treating their customers fairly – after all, in most cases of MPS investing, it is the adviser who accepts suitability responsibility.

“It may be buried deep in the small print but we do not recall seeing any DFMs detailing their approach to cash balances.

What is important and what should get all asset managers – and advisers – sitting up and taking notice is that putting these infractions right is a costly business.”

As each step along this regulatory pathway evolves, you can almost sense a feeling of frustration within the FCA in that, if the foundation of doing business with consumers is to treat them fairly, then principles, procedures, systems and governance should already have been in place to give the best chance of delivering good client outcomes.

Coincidence or not, we have over the last couple of weeks seen Rathbones undertaking a Skilled Persons Review following ‘engagement’ with the FCA. The review identified areas for improvement within the firm’s wealth management business regarding implementing and embedding Consumer Duty as well as certain aspects of its compliance and governance.

What is important and what should get all asset managers – and advisers – sitting up and taking notice is that putting these infractions right is a costly business. Rathbones is undertaking a two-year programme addressing the recommendations of the review, which in itself will be a costly process – not to mention the lost revenue from voluntarily pausing the onboarding of clients that require ‘enhanced due-diligence’.

Furthermore, Rathbones has ceased charging fees on cash held in portfolios and has also commenced a review of certain aspects of its pricing in its commitment to delivering fair value for its clients.

What we can conclude from all this is the FCA is taking the treatment of clients very seriously and the lens of regulation is very much on this sector. Not taking this just as seriously as a business could be very costly indeed.

Source of frustration

Rathbones ceasing to take fees on cash balances in portfolios puts the spotlight on one area where there is little transparency and has the potential be viewed as unfair charging. As such, this is a good example of a source of frustration to the FCA.

At the turn of 2024, a ‘Dear CEO’ letter was sent out to investment platforms and Sipp operators, essentially requesting they get their houses in order and treat customers fairly in terms of charging on cash balances. It was not directed at DFMs specifically but, as Defaqto pointed out at the time, it was an obvious read-across and should also have been addressed by any product provider that dealt with client cash balances.

So, what is the scale of this particular issue in DFM world? At its heart, the question comes down to where charges can be applied on cash balances and whether they are reasonable?

There are arguably three points of potential charging here. First, we know some custodians take a slice of the interest earned – particularly if they are the ones administering the cash balances alongside the assets. For those solutions accessed through adviser platforms, we would also consider the platform as the custodian – remember it is two years since the ‘Dear CEO’ letter!

The second area relates to asset managers, where they take ‘a haircut’ in lieu of the cost of managing the cash. Again, how much is reasonable? The third – and perhaps more common – area of charging is subjecting cash balances to the annual management fee.

Over the years, Defaqto has heard arguments justifying charges on cash balances – and there are undoubtedly one or two grey areas. It does cost to administer cash balances – but, again. how much is fair? If a portfolio manager ups the cash balance as a defensive move and as a result saves the client money, is a fee justifiable?

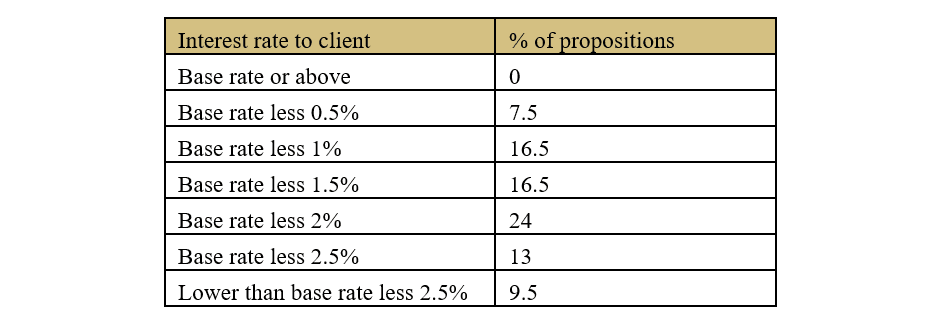

Defaqto periodically collects the current rate clients are paid on cash balances from DFM firms – and there is quite a range, as you can see from the following table:

Almost half pay interest at base rate less 1.5% or less. If DFMs are also charging an annual management fee, we would suggest these charges could be viewed as excessive. We only have to think what rate we would get if we wandered down to the local building society with a couple of thousand pounds. With a bit of searching, we could potentially achieve a better rate than all the above.

It may be buried deep in the small print but, here at Defaqto, we do not recall seeing any DFMs detailing their approach to cash balances. As such, we would argue this issue is symptomatic of why the FCA is frustrated and feels a review of the MPS market is required.

Nor is it just asset managers that need to sit up and take the matter seriously: advisers also have to ensure their clients are being treated fairly – especially when investing in MPS, where suitability responsibility tends to fall to them. The cost to Rathbones is a salutary lesson to all.

There are more than 30 detailed questions in the FCA’s MPS multi-firm review survey and we can be certain the regulator will address any issues arising as they seek to ensure investors receive good outcomes. Be ready!

Andy Parsons is head of insight at Defaqto