Recent articles have in essence focused on some of the aspects advisers will – or at least should – be asking when undertaking due-diligence. This one turns its attention to another important factor when considering an appropriate DFM – taking a closer look at assets under management or ‘AUM’.

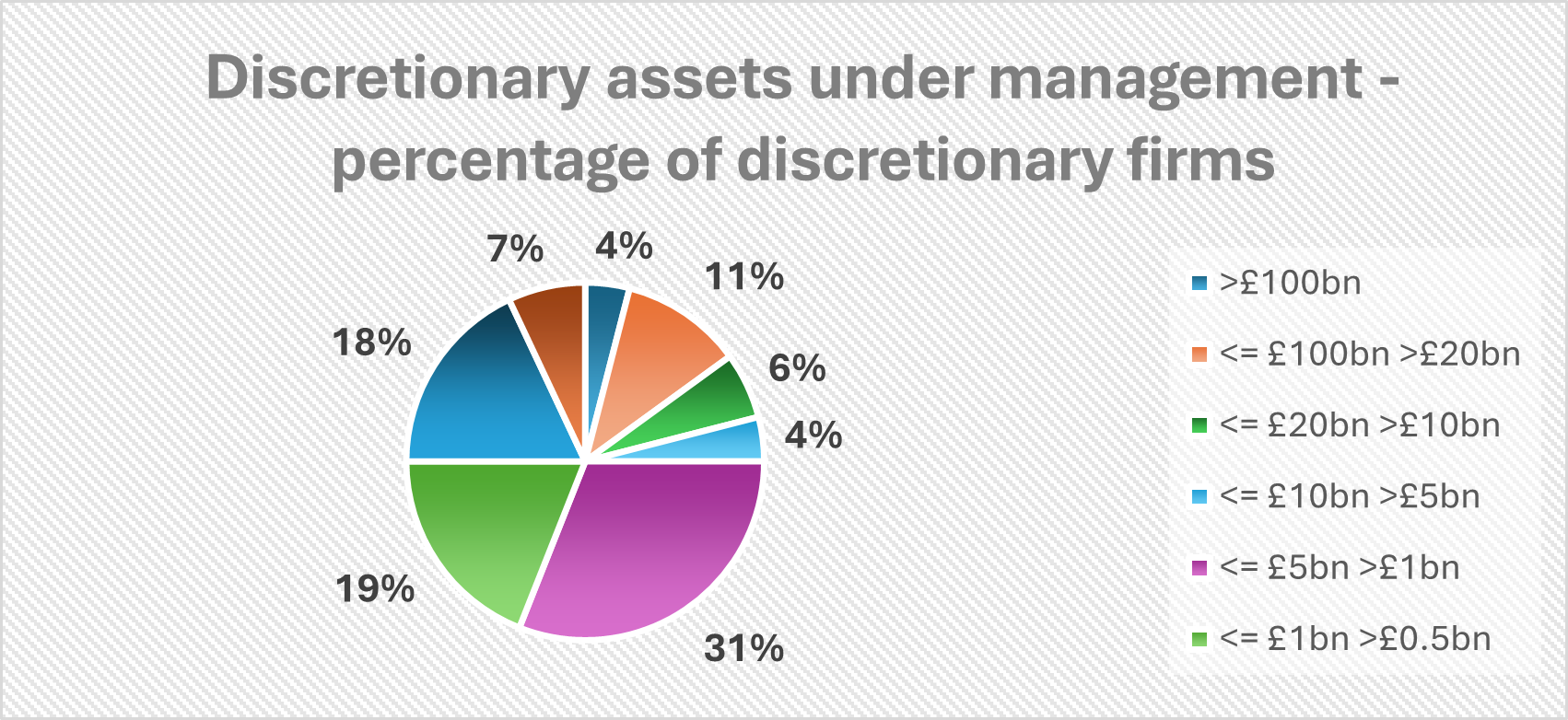

There are actually three levels of assets under management that bear a closer look when undertaking due-diligence: ‘discretionary AUM’; ‘group AUM’; and ‘portfolio AUM’. So, why would an adviser look closely at each of these numbers? Let’s zoom in on discretionary assets under management first.

The following chart showcases the percentage of firms split by how much discretionary money they are running. There are only a handful of companies that are running what. in the fund management world, would be considered ‘significant assets’. As the figures clearly show, only 25% of the firms currently run more than £5bn, while, at the other end of the spectrum, 25% run less than £0.5bn.

“While there is no compulsion to provide Defaqto with data, it does raise questions as to why all other data requests are completed – but not this one.

Source: Defaqto. Please note: A small number of firms do not provide any AUM data to Defaqto. These are primarily firms that have retreated back into the private client market

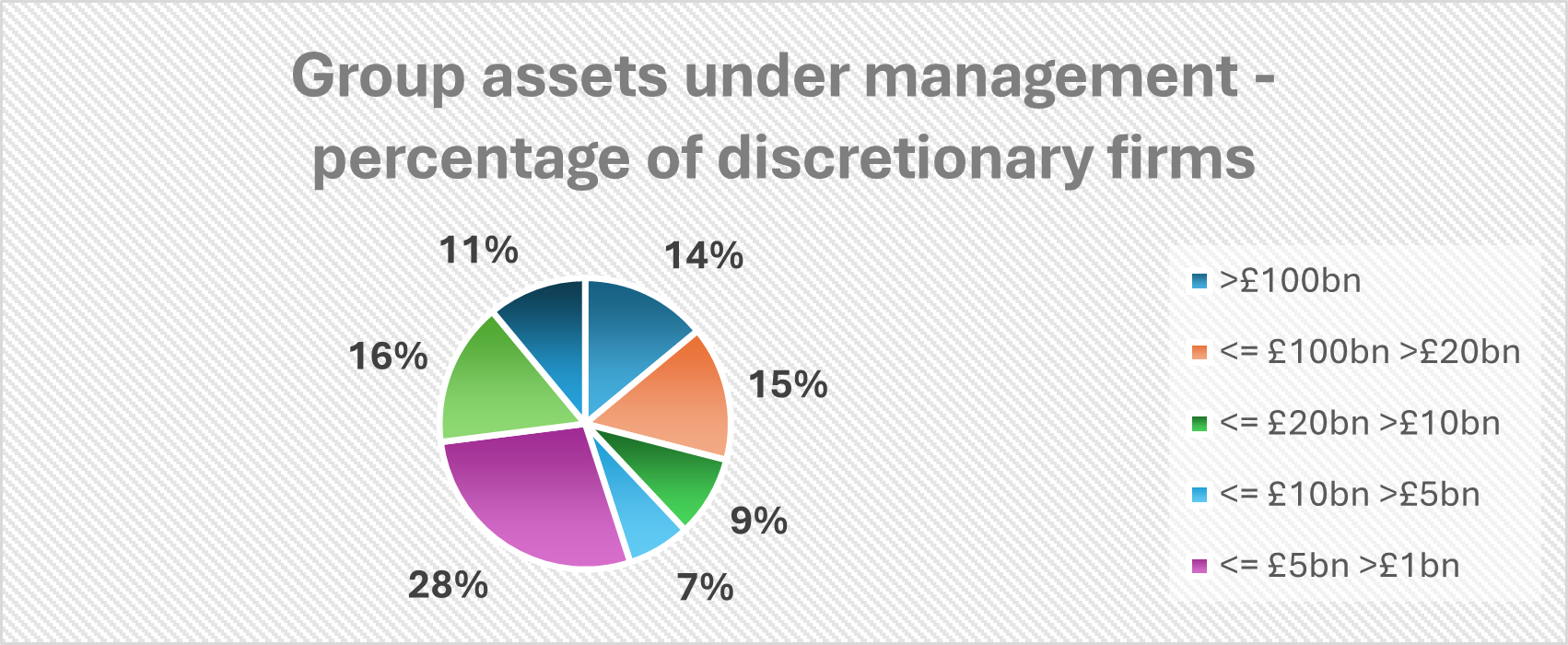

It is with this in mind that advisers should also be looking at ‘group AUM’ – as detailed next:

Source: Defaqto. Please note: A small number of firms do not provide any AUM data to Defaqto. These are primarily firms that have retreated back into the private client market

There are several firms that are relatively new to the discretionary market – although many of these are subsidiaries of much bigger asset managers. Apart from a relatively small handful, most DFMs have only been targeting the retail market during the period since the Retail Distribution Review. Many have yet to gain traction with advisers as they have only relatively short periods of performance history.

As a result, it is not unusual to see firms with relatively low discretionary AUM and, in such situations, it is a useful proxy to see what the parent companies’ AUMs are. If they are significant, it points to potential support in terms of covering early years’ lack of profitability, shared research and shared administration. That said, such support is not guaranteed – and each case should be looked at on its merits and assurances sought.

Indeed, there is an almost contradictory view to this – in that firms whose sole business is discretionary management could be seen to have a greater determination and focus to succeed in this arena where there are no other business lines to support the firm.

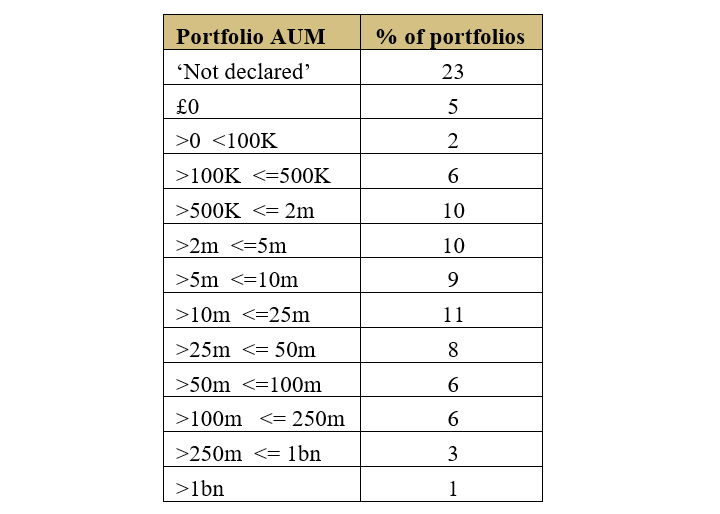

Let’s now turn our attention to AUM figures within individual portfolios – focusing solely on those that are available through adviser platforms, since this all but eliminates firms that have retreated back into the world of ‘private client-only’.

Depending on the adviser and requirements of the client, there could be a preference for portfolio size, whether big or small. At Defaqto, we regularly collect portfolio-size data and, as is to be expected, there is a wide range of portfolio sizes. This is encapsulated in our next table:

Source: Defaqto

Individual portfolio sizes are notoriously difficult to collect. Setting aside potential lags in data receipt due to relying on platform MI and how often that is produced, the figure that stands out here is the 23% of portfolios that have not declared what their AUM is.

And, while there is no compulsion to provide Defaqto with data, it does raise questions as to why all other data requests are completed – but not this one.

We all know that, in the main, DFMs launch ranges of portfolios that are designed to appeal to as wide a client base as possible. This often means including portfolios in the range that would only appeal to the ultra-defensive or the extreme risk-takers at either end of the risk scale. This is done in the knowledge that uptake will be low – or even non-existent – but might attract business elsewhere on the risk scale.

So, why hide it? We note from the numbers above that 5% of portfolios are content to show a zero uptake. What is more, there is an unfortunate ‘ripple effect’ for those firms that chose not to declare, in that they will often not declare sizes for other portfolios in their range.

For those advisers who feel that portfolio size is important to their due-diligence process, referring to factsheets may be another source of information – though, as we have discussed previously, we have found that in most cases the information is not published there either.

An adviser could enquire directly to the DFM, but this is probably a step too far for an adviser firm trying to be as efficient as possible. Advisers should not be expected to have to ‘dig’ for information that should be freely and easily available.

We would hope and expect the regulator would address some of these lingering transparency issues and encourage firms to provide easy access to relevant due-diligence data such as detailed AUM figures.”

We know that, given the strength and demand for MPS portfolio solutions, the FCA are embarking on a review of the MPS market. In order to harmonise as much as possible with the more established multi-asset fund market, we would hope and expect the regulator would address some of these lingering transparency issues and encourage firms to provide easy access to relevant due-diligence data such as detailed AUM figures.

While appreciating the challenges and potential difficulties to provide such data on a monthly basis, there can be little argument as to why it cannot be done on, say, a quarterly basis. What is there to hide?

As to whether portfolio size is actually a clear indicator of viability or exposing clients to concentration risk, that is a trickier question and down to the judgement of the adviser.

For platform portfolios, much of the administrative cost is taken on by the platform and ultimately paid for by the client through platform charges. In most cases, each portfolio in a range will contain the same underlying holdings, albeit with different weightings to increase or decrease risk.

Broadly then, it is probably more informative to look at AUM for the range rather than individual portfolios. That said, there are still costs involved for each portfolio – primarily from a marketing point of view, such as inclusion in brochures, factsheets, risk ratings and so on, but also costs involved in continuing to manage the portfolios. And should the FCA review dictate enhanced disclosure, there are likely to be more costs involved, perhaps making some of the portfolios at the extremes of risk less viable.

Overall, it is important to look at AUMs in context, using your experience and making a judgement on the relevance of each number.

Andy Parsons is head of investment at Defaqto