“The greatest danger in times of change is not the change itself; it is acting with yesterday’s logic.” Peter Drucker

For an asset class that has spent much of the past five years failing to deliver returns, diversification or protection, fixed income remains surprisingly firmly embedded in client portfolios. This persists despite a prolonged period of underperformance – particularly laid bare for cautious investors in 2022 when bonds’ vulnerability was fully exposed.

Investors continue to cling slavishly to the textbook idea of equity-bond diversification and the well-worn 60/40 model – kept alive as much by persuasive marketing as by results. Markets, however, appear not to have read the same material.

Bonds have traditionally been held for good reason: they are meant to provide income, preserve capital and, critically, diversify equity risk – thereby forming the defensive core of portfolios designed to protect investors’ hard-earned wealth and help shield portfolios during times of extreme equity stress.

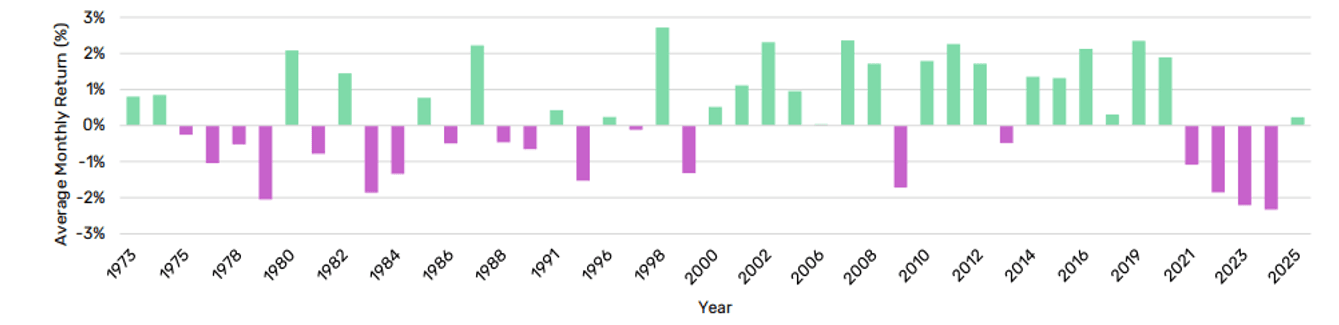

The assumption they continue to do so, however, appears to persist more out of habit than evidence. The following chart shows that, as the interest rate outlook changed in 2021, the correlation between equities and bonds ceased to be strongly inverse. The returns from bonds in March 2026 look set to show a positive correlation once again – all of which clearly calls into question one of the central pillars of traditional portfolio construction.

Average monthly UST return when S&P500 return is <-3%

“The question is not whether bonds have historically worked or whether they are working now – it is why they continue to be relied upon so heavily, even as the evidence challenges the role they are expected to play.

Source: Man Group, February 2026

While liquid alternatives are often dismissed for a variety of reasons – cost, performance, complexity or a few well-known failures – bonds appear to enjoy a far more forgiving assessment, despite a much longer and more consistent record of disappointment. The question is not whether bonds have historically worked or whether they are working now – it is why they continue to be relied upon so heavily, even as the evidence challenges the role they are expected to play.

So why are allocations still So blinkered? Looking back over the past five years provides a useful lens through which to assess how different asset classes have behaved in practice, rather than in theory. Spoiler alert: the results are not especially flattering for fixed income.

Cash has delivered a steady and positive return over the period, as our next chart shows. By contrast, most bond asset classes have struggled to generate meaningful returns, with many failing even to keep pace. UK government bonds have produced negative outcomes while the Bloomberg Global Aggregate index has also disappointed. Even corporate bonds – often positioned as a more attractive segment of the market – have delivered only modest gains.

Five years of hurt

Source: FE Analytics. Total return over five years to 31/03/26

For an asset class expected to provide stability, income, and protection, such numbers should, at the very least, make for uncomfortable viewing. And yet, despite this, bonds remain one of the most widely held components of portfolios, particularly for lower-risk investors. That raises a more fundamental question:

* Is it because of high confidence in future returns…

* … a belief their diversification properties will reassert themselves …

* … or simply the continued influence of longstanding assumptions that have yet to be fully challenged?

The reality over the past five years is difficult to ignore. In many cases, investors would have been better served by a simple barbell of cash and equities – excluding bonds altogether – and paying lower fees for the privilege. The IA Mixed Investment 0–35% Shares sector, which is dominated by exposure to fixed income assets, highlights this clearly, having lagged even cash over the period.

The outcomes are clear – the logic behind current allocations, rather less so. At the same time, liquid alternatives, when considered at the aggregate level rather than through individual fund selection, have delivered positive outcomes over the same period, drawing on a broader and more flexible set of return drivers.

Failed test

If the past five years challenge the strategic case for bonds, more recent events raise questions about their behaviour when it matters most. Periods of market stress tend to expose underlying assumptions. March was one such period.

It was a challenging time across asset classes, with volatility rising sharply and correlations behaving in less predictable ways. As our next table show, however, bonds – typically expected to provide a degree of protection in such environments – struggled alongside other risk assets.

Selected IA sector returns – March 2026

Source: FE Analytics. Total return from 01/03/26 to 31/03/26

Across the corporate bond universe, outcomes were both negative and remarkably consistent. Corporate bond and gilt funds both delivered losses across the board, with no funds in either sector producing a positive return. The range of outcomes was relatively narrow, reflecting a common exposure to the same underlying drivers – a somewhat uncomfortable result for an asset class relied upon for both defence and diversification.

By contrast, outcomes within the absolute return universe were more varied. Some strategies struggled – particularly those with exposure to rates and macro positioning and those with higher risk profiles. Others were more resilient and, indeed, a number were able to navigate the environment more effectively.

This variation is often presented as a weakness. In reality, it reflects something quite different. Absolute return is not a single trade – it is a collection of different strategies responding in different ways to the same set of conditions.

In other words, it should be viewed as a broad, diversified basket of exposures – not a single fund to be selected and judged in isolation. When bonds struggle, they tend to struggle together. When absolute return strategies struggle, they do so for different reasons and, most importantly, not always at the same time.

Judging the wrong issue

One of the more predictable responses to periods like March is to point to the absolute return sector delivering negative returns and conclude that the asset class “doesn’t work”. It is an easy conclusion to draw. It is also a flawed one.

Absolute return has never been positioned as an asset class that should deliver consistent positive returns in every month, nor one that should be inversely correlated to equities in all environments. That has never been the objective. And yet, it is often judged as though it were.

What is less frequently acknowledged is that, in the same environment, bonds, which are widely assumed to provide downside protection, not only failed to protect, but in many cases delivered more consistent losses across the board.

There is a clear asymmetry in how these outcomes are interpreted. When absolute return funds lose money over a short period, it is taken as evidence the approach is fundamentally flawed. When bonds do the same, often more uniformly, it is viewed as an unfortunate but temporary deviation.

Over longer periods, however, the evidence is increasingly difficult to ignore. Absolute return, when viewed as a diversified opportunity set, has delivered stronger outcomes than bonds across a range of metrics – not just returns, but volatility, drawdowns, and the balance of positive and negative periods.

Selected IA sector returns – Five years to end-March 2026

Source: FE Analytics. Total return from 31/03/021 to 31/03/26

The data makes this clear. When approached as a diversified allocation, absolute return has delivered stronger and more consistent outcomes than bonds:

* Over five years, 97% of targeted return funds delivered a positive return …

* … for corporate bonds, that figure is just over 50%.

What is more, that is before any attempt is made to improve outcomes through manager selection. And yet, this is rarely how the debate is framed. Instead, periods of short-term weakness are often used to dismiss the entire category, while bonds continue to benefit from a far more optimistic narrative.

As a consequence, allocation to liquid alternatives remains woefully low in client portfolios – and, at some point, it is reasonable to ask whether this reflects a genuine shift in fundamentals, or simply a reluctance to move on from a familiar framework.

A misunderstood asset class

The mistake made with absolute return is rarely the strategy itself, but rather how it is used. We do not expect a single equity or a solitary bond to represent the entirety of their respective markets – and so we diversify across sectors, geographies and issuers to mitigate specific risk. Absolute return must be viewed through this same lens.

Selecting a single absolute return fund and expecting it to perform in all conditions is no more robust than selecting a single bond and expecting it to represent the entire fixed income market. There is no silver bullet in this space – while the sector contains many excellent strategies, it also includes those that will inevitably encounter periods of friction. Relying on a single fund is an exercise in unnecessary concentration.

There is, however, clear scope for wealth managers to sift through this universe and build a robust portfolio of highly diversified strategies that can deliver strongly over time. Even with a reluctance to do this, there are diversified fund of funds options available that act as a single, one-stop solution for allocating towards the asset class.

By moving away from a reliance on one single fund and instead creating a diversified allocation, investors can better capture the true benefits of the asset class. While a blended basket will not guarantee a positive return in every ‘down’ market, it will certainly deliver a more resilient portfolio profile, one with the genuine ability to outperform.

Bonds have played a central role in portfolios for decades, but their ability to deliver on that mandate can no longer be taken for granted. While liquid alternatives are not a substitute for every asset class, nor a guaranteed hedge in all conditions, they represent a more adaptive approach to portfolio construction – one that is less reliant on a single set of assumptions holding true.

The question, therefore, is not whether bonds should be removed entirely, but whether their role and weighting still reflect the realities of the current environment. Investors often say they do not trust absolute return yet, when the evidence of the past five years is laid bare, a more relevant question emerges: why do we continue to cling to a shield that has already shattered, while avoiding the very tools better suited to the world we now inhabit.

Ian Willings is a portfolio manager and partner at Apollo Multi Asset Management, experts in researching and investing in absolute return and liquid alternative strategies. CIO, Steve Brann, is the author of Absolute Vision, a book that sets out the thinking behind the firm’s strategy and looks to demystify the asset class for a wider audience. For a free copy, please contact info@apollomam.co.uk